40% off TNW Conference!

The rate the company calculated the policyholders should be paying is called the indicated premium in its filing.

(In this paper, well call it the ideal price.)

But Allstate didnt propose adjusting rates to those ideal prices.

Allstate called the rates they wanted to charge the selected premium.

(In this paper, well call it the transition price.)

Instead, Allstate capped their transition price increases at 5.02 percent.

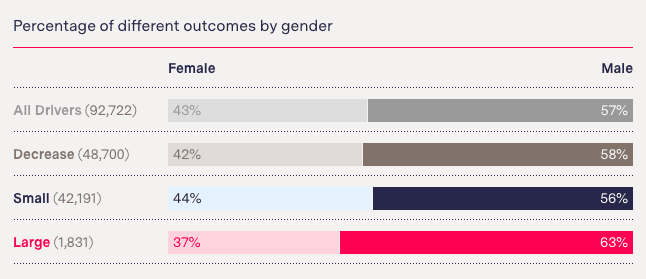

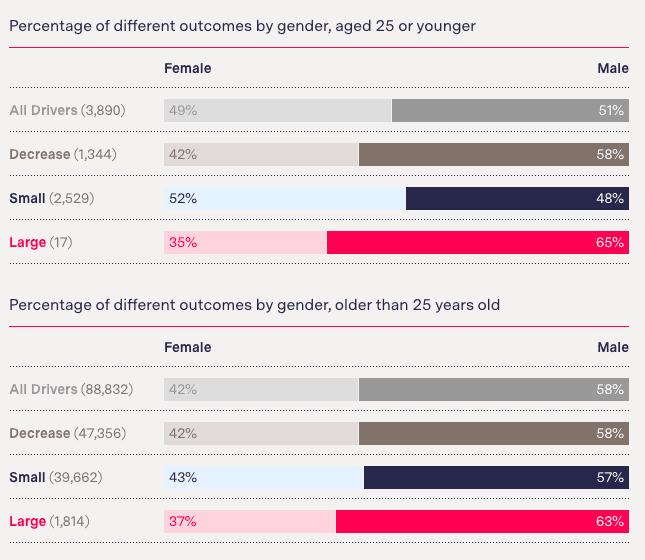

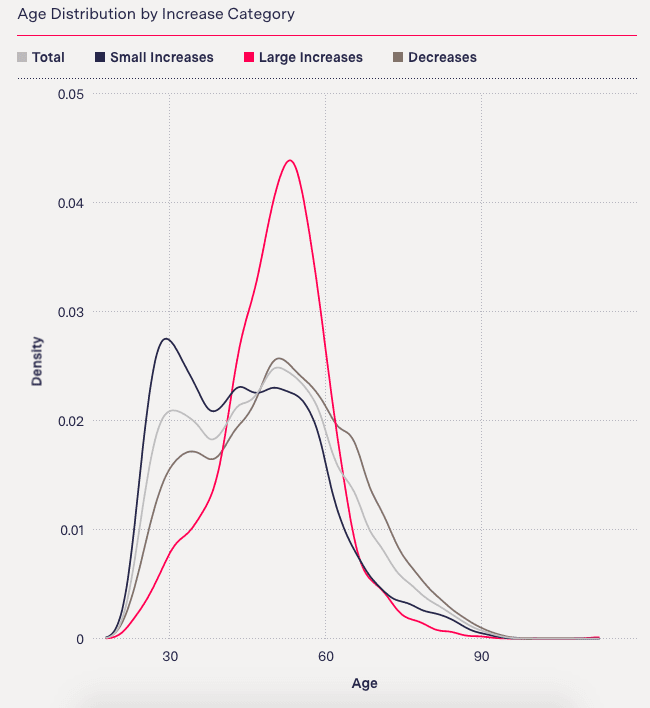

We found that customers who would have received massive rate hikes under Allstates plan were disproportionately middle-aged.

Those with massive rate hikes were also disproportionately male.

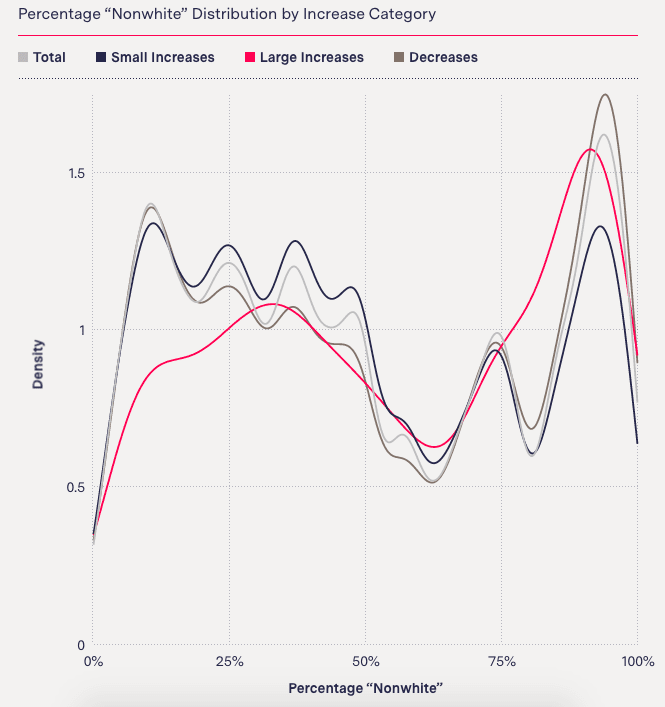

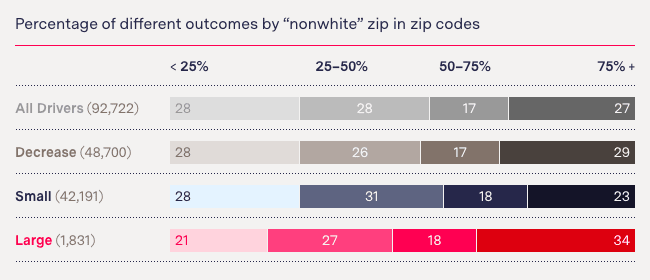

They were also disproportionately living in communities that were more than 75 percent nonwhite.

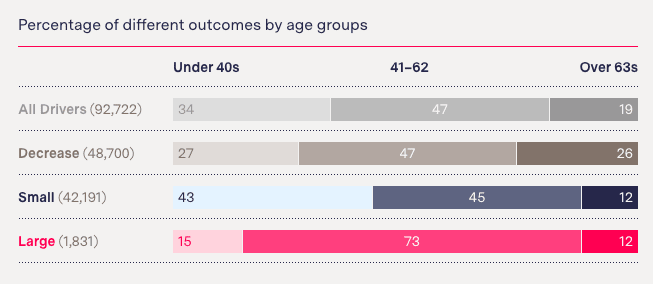

Customers aged 63 and older were disproportionately affected by the lack of meaningful discounts.

There are limitations to our analysis.

The proposal was never put into use in Maryland.

Insurers regularly submit rating plans to regulators.

Unlike the techniques of the past, these methods are not straightforward.

The consumer group accused Allstate of using illegal techniques to shift rates.

Nevertheless, Allstate was undeterred in its push toward setting rates based on retention.

Maryland regulators said the use of CGR results in rates that are unfairly discriminatory.

Allstate withdrew proposals in some other states, including Louisiana and Rhode Island after regulators asked pointed questions.

In its letter to Georgia regulators, Allstate defended its practices, stating that TAN is not price optimization.

The details of its algorithm are not included in many filings to state regulators.

In some filings, Allstate includes information about the algorithm in an exhibit that is kept from the public.

Of the 92,792 entries, 70 had zip codes not included in the ACS data, and were removed.

CGR is based in part on proprietary retention models.

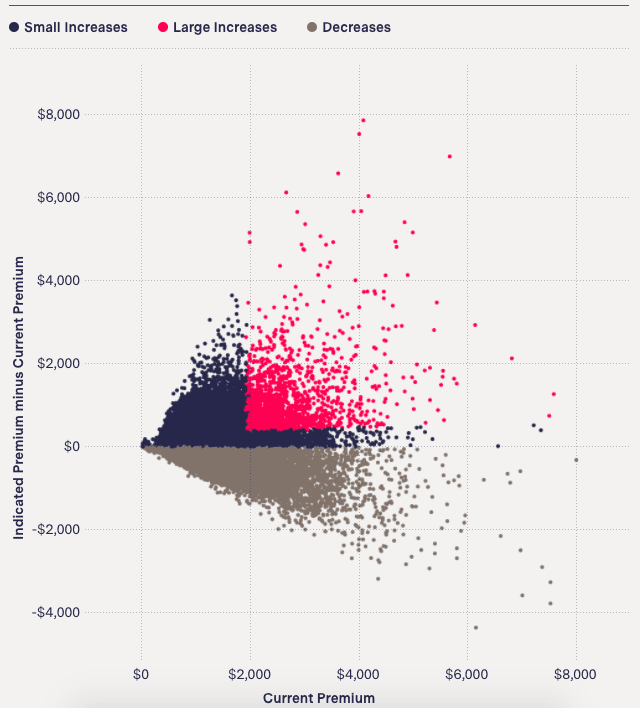

Consider two 32-year-old men in Prince Georges County.

One was paying Allstate $2,617.42 for six months of coverage, the other, $814.48.

They needed a 21.7 percent increase and a 21.8 percent increase, respectively, to reach their ideal prices.

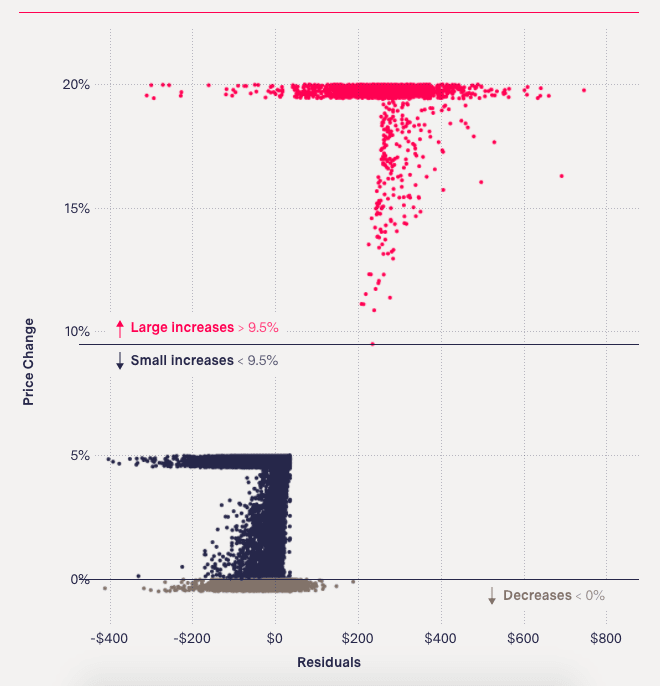

The cutoff prices had fuzzy borders.

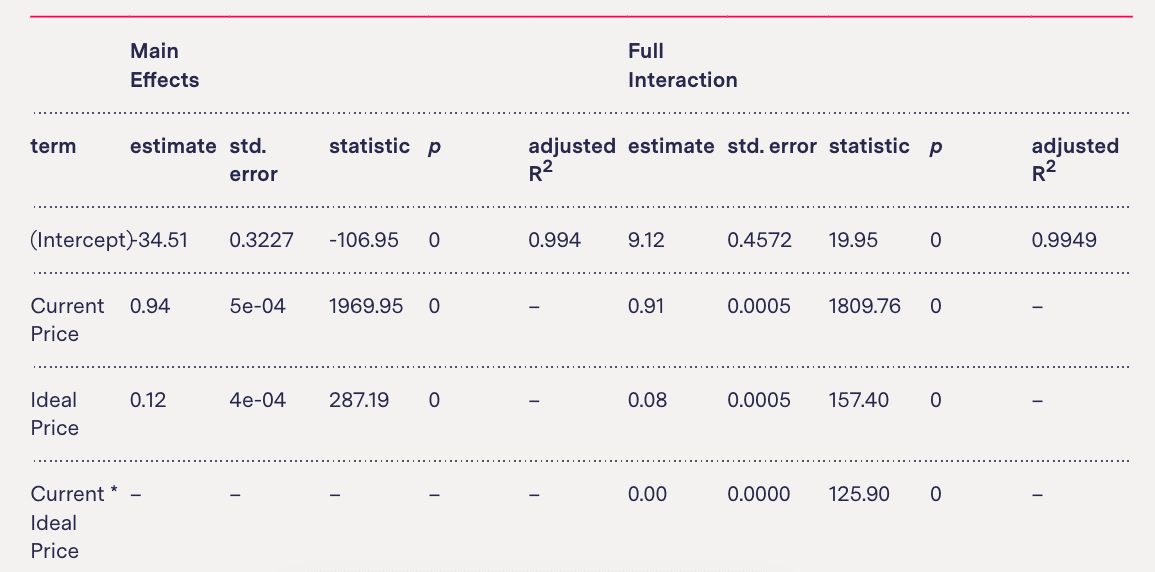

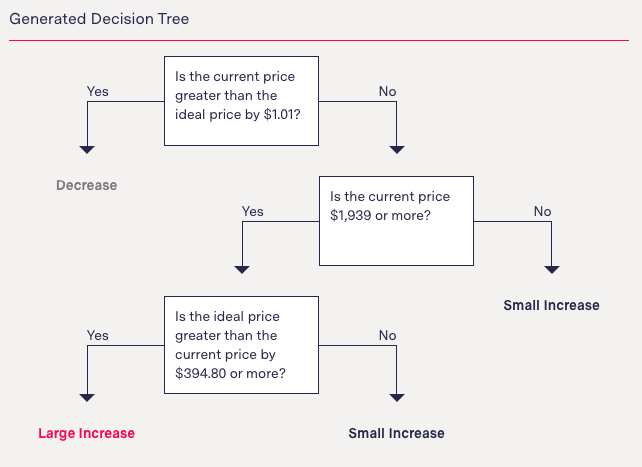

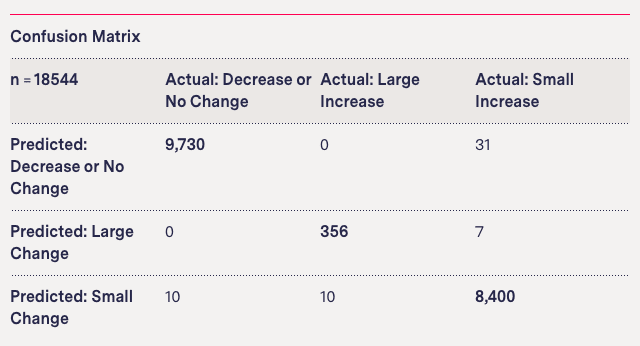

The model output is contained in the table below.

We fit a decision tree model with a depth of three using a five-folds cross validation.

Our simple model was able to correctly categorize the testing dataset 99.69 percent of the time.

The sample size for men who are under 25 and in the large increase pool isn=11.

Of the 16,570 customers in that age group, 70.8 percent were owed discounts.

Racial composition of zip code

The Maryland dataset contains information about the zip code of each policyholder.

We then examined the relationship of race to the price change groups.

We split the data into four buckets based on the percentage of nonwhite population living in their zip code.

The Maryland proposal, the statement said, aimed to minimize customer disruption and provide competitive prices.

In emails Jones insisted the insurer had withdrawn the filing.

Maryland Insurance Administration spokesperson Joseph Sviatko said Allstate withdrew the filing only after the state emailed the denial letter.

He said the designation makes no practical difference internally.

The first time we were told it didnt exist.

In addition, the proposed plan would have disproportionately affected different groups.

So were middle-aged drivers and men.